Step-by-Step Instructions

When an emergency occurs, adrenaline makes it difficult to think clearly. Following a structured, sequential approach to filing a claim guarantees that you protect your safety while securing the financial reimbursement you deserve. Treat this process methodically, documenting every single detail along the way.

Phase 1: Secure the Environment and Ensure Safety

Never prioritize property over human life. If a fire breaks out, evacuate immediately and call 911. If a pipe bursts and floods your living room, act fast to mitigate further destruction; immediately turn off the main water valve if you can reach it safely. Safety Warning: Never enter a room with standing water if the electricity remains active. Call your property manager or local utility company to cut the power before you attempt to salvage any wet belongings.

Phase 2: Alert the Authorities

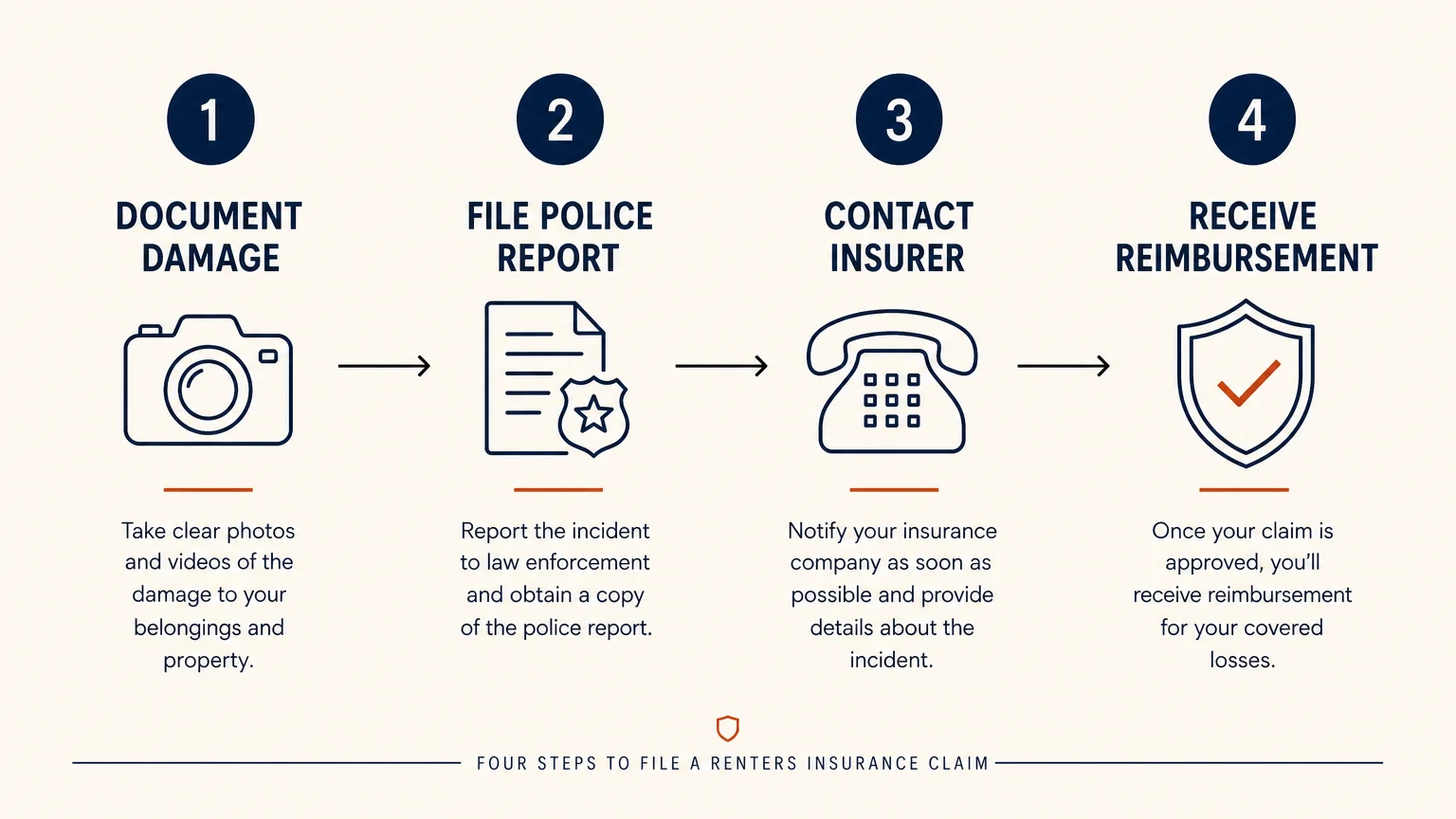

Insurance carriers require an official paper trail, especially when dealing with theft protection or malicious vandalism. If a burglar breaks into your apartment or steals your bicycle from a public rack, call the police immediately. Do not clean up broken glass or reorganize your belongings until the responding officers file an official police report. You must provide this report number to your insurance adjuster to validate your claim.

Phase 3: Formalize the Damage Record

Once the authorities clear the scene, begin your preliminary damage assessment. Take dozens of brightly lit photographs from multiple angles. Capture close-ups of ruined electronics, water-stained upholstery, and smashed windows. Cross-reference these damage photos with your pre-recorded digital home inventory to create a comprehensive list of lost or ruined items.

Phase 4: Initiate the Claim with Your Carrier

Contact your insurance agent or use your carrier’s mobile app to initiate the claim within 24 hours of the incident. Provide the date, time, and a factual summary of the event. Avoid speculating about the cause of the damage; simply stick to the concrete facts. The carrier will assign a dedicated claims adjuster to your case.

Phase 5: Cooperate and Negotiate

The insurance adjuster will review your photos, the police report, and your inventory list. They may schedule an in-person visit to inspect severe property damage. Provide them with copies of your original receipts to prove the value of your lost items. Review the initial settlement offer carefully before accepting it; if the payout seems exceptionally low, present your professional appraisals to negotiate a fairer reimbursement based on your specific renter rights.

Leave a Reply

You must be logged in to post a comment.